On July 31, 2025, the Ministry of Economy and Finance (MOEF) released the 2025 proposed tax law amendment proposals (the Proposal(s)). The MOEF stated that the Proposals are intended to strengthen the tax revenue base by promoting economic growth and rationalizing the tax system. The core aims of the Proposals are: (i) providing effective tax support for technology-driven growth; (ii) building an inclusive tax system that fosters growth for all; and (iii) reinforcing the tax revenue base to ensure fair growth. If approved during the regular National Assembly sessions in 2025, the Proposals should become effective from January 1, 2026, unless otherwise specified.

Some of the key items of the Proposals that may be of interest to foreign invested companies and foreign investors are as follows.

■ Corporate Income Tax Law, Individual Income Tax Law, Securities Transaction Tax Law

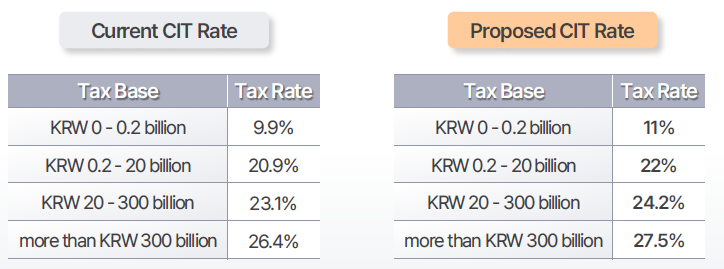

1. Increase in Corporate Income Tax Rate (Article 55(1) of the Corporate Income Tax Law)

2. Increase in Securities Transaction Tax Rate (Article 5 of the Presidential Decree of the Securities Transaction Tax Law)

3. Lowering of the Capital Gains Tax Threshold for Listed Stocks (Article 157(1)-(2) of the Presidential Decree of the Individual Income Tax Law)

4. Increase in Education Tax Rate (Article 5 of the Education Tax Law)

5. Expansion of Taxation on Dividends from Capital Reserve Reductions (Article 26-3 of the Presidential Decree of the Individual Income Tax Law)

6. Clarification of Domestic Source Income of Foreign Companies (Article 93 of the Corporate Income Tax Law)

7. Improvements to the Application of the Foreign Tax Credit for Indirect Investment

8. Introduction of Penalties for Failure to Submit Status Reports on Liaison Offices of Foreign Companies (Article 125 of the Corporate Income Tax Law)

9. New Requirement to Submit Applications for Treaty-Based Reduced Tax Rates for Non-Residents (Article 156-6 of the Individual Income Tax Law, Article 207-8(8) of the Presidential Decree thereto, Article 98-6 of the Corporate Income Tax Law, Article 138-7(8) of the Presidential Decree thereto)

10. Expansion of the Exit Tax to Overseas Stocks (Article 118-9 through 118-18 of the Individual Income Tax Law)

■ International Tax Coordination Law

11. Introduction of Domestic Minimum Top-up Tax (DMTT) under the Global Minimum Tax Framework (newly established Article 73-2 of the International Tax Coordination Law)

12. Additional Documentation Requirement for Tax Refund Claims Arising from Transfer Pricing Adjustments (Article 6(2) of the International Tax Coordination Law)

13. Inclusion of Investment Trusts within the Scope of Residency Certificate Issuance (Article 41 of the International Tax Coordination Law)

■ Special Tax Treatment Coordination Law

14. Introduction of Separate Taxation on Dividend Income from High-Dividend Companies (newly established Article 104-27 of the Special Tax Treatment Coordination Law)

15. Introduction of Tax Exemption for Domestic Investment Income of the Bank for International Settlements (BIS) (Article 21(4), (5), and (6) of the Special Tax Treatment Coordination Law)

16. New Tax Deferral for In-Kind Contributions of Foreign Subsidiary Shares to Foreign Companies (Article 38-3 of the Special Tax Treatment Coordination Law, Article 35-5 of the Presidential Decree thereto)

■ Corporate Income Tax Law, Individual Income Tax Law, Securities Transaction Tax Law

1. Increase in Corporate Income Tax Rate (Article 55(1) of the Corporate Income Tax Law)

To address the erosion of the tax revenue base following the previous administration’s corporate tax cuts, the Proposals would provide for a 1% increase in each corporate income tax (CIT) bracket, thereby restoring the rates to their 2022 levels.

If enacted, the revised rates will apply to fiscal years commencing on or after January 1, 2026. This includes the 10% local income tax.

2. Increase in Securities Transaction Tax Rate (Article 5 of the Presidential Decree of the Securities Transaction Tax Law)

The securities transaction tax (STT) rate on listed stocks (KOSPI and KOSDAQ) had previously been reduced in connection with the planned (but postponed) introduction of the financial investment income tax. However, with the repeal of the financial investment income tax following prolonged policy debate, the Proposal includes a 0.05 increase in the STT rate, restoring it to the 2023 level.

Meanwhile, the 0.35% tax rate on unlisted stock transactions will remain unchanged, as the Proposals do not provide for any adjustment to this rate.

If enacted, this Proposal will apply to share transfers made on or after the effective date of the amended Presidential Decree of the Securities Transaction Tax Law.

The tax base for STT is the gross transfer price or FMV of the shares transferred.

| STT Rate |

| Type |

FY2023 |

FY2024 |

FY2025 |

Proposed |

| KOSPI |

0.20% |

0.18% |

0.15% |

0.20% |

| KOSDAQ * |

0.20% |

0.18% |

0.15% |

0.20% |

| KONEX ** |

0.10% |

0.10% |

0.10% |

0.10% |

* Including 0.15% Special Rural Development Tax (SRDT). The SRDT does not apply to KOSDAQ-and KONEX-listed securities

** STT Rate for stocks traded on KONEX market remains unchanged.

3. Lowering of the Capital Gains Tax Threshold for Listed Stocks (Article 157(1)-(2) of the Presidential Decree of the Individual Income Tax Law)

Under the current law, domestic individual shareholders of a Korean publicly traded company are generally not subject to capital gains tax unless: (i) their shareholding ratio is at least 1% for KOSPI-listed companies, 2% for KOSDAQ-listed companies, or 4% for KONEX-listed companies; or (ii) the market value of their shares is at least KRW 5 billion. (Article 157(1)-(2) of the Presidential Decree of the Individual Income Tax Law).

While the shareholding thresholds are not changed under the Proposals, they seek to lower the market value threshold from KRW 5 billion to KRW 1 billion, thereby restoring the standard that applied prior to the 2023 tax law amendment.

If enacted, this Proposal will apply to transfers made on or after the effective date of the amended Presidential Decree of the Individual Income Tax Law.

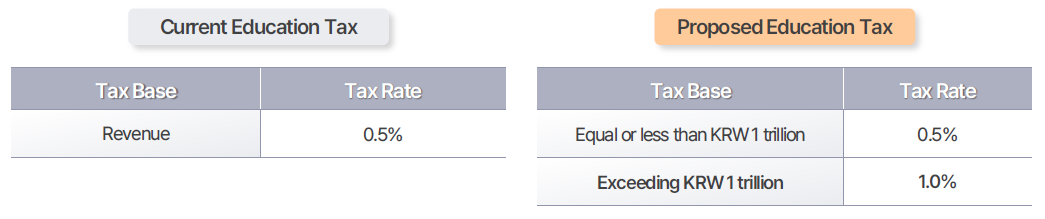

4. Increase in Education Tax Rate (Article 5 of the Education Tax Law)

Under current law, the financial and insurance industries are exempt from VAT. In place, they are subject to an education tax of 0.5% of revenue which has remained largely unchanged since the education tax was introduced in 1981.

To enhance tax equity in light of the sustained growth of these industries, the Proposals would introduce a new tax bracket for revenue exceeding KRW 1 trillion. For large financial and insurance companies within this bracket, the top marginal education tax rate is expected to double from the current 0.5% to 1%.

If enacted, this Proposal will apply to tax periods beginning on or after January 1, 2026.

5. Expansion of Taxation on Dividends from Capital Reserve Reductions (Article 26-3 of the Presidential Decree of the Individual Income Tax Law)

Under current law and tax ruling, dividends distributed from capital reserve reductions are treated as follows: i) For corporate shareholders, the dividend amount is first deducted from the acquisition cost of the shares (Article 41 of the Corporate Income Tax Law; Article 72(5)1 of the Presidential Decree of the same law). Any excess over the acquisition cost is recognized as taxable income of the corporate shareholder (Article 18(8) of the Corporate Income Tax Law); and ii) for individual shareholders, the dividend amount is likewise deducted from the acquisition cost of the shares (MOEF Financial Taxation Division-439, 2024.10.23.). However, any excess over the acquisition cost is not currently subject to taxation as dividend income (Article 26-3(6) of the Presidential Decree of the Individual Income Tax Law).

The Proposals would narrow the scope of non-taxation on capital reserve reduction dividends, such that major shareholders (i.e., major shareholders of listed companies subject to capital gains tax) and shareholders of unlisted companies would be subject to dividend income tax on the portion exceeding the acquisition cost of the relevant shares. In other words, under the Proposal, shareholders subject to capital gains tax on stock transfers would also be subject to dividend income taxation, in the same manner as corporate shareholders, when receiving dividends from a reduction of capital reserves.

If enacted, this Proposal will apply to dividends received on or after the effective date of the amended Presidential Decree of the Individual Income Tax Law.

6. Clarification of Domestic Source Income of Foreign Companies (Article 93 of the Corporate Income Tax Law)

1) Clarification of the scope of Korean-source other income: gifts of domestic assets to foreign companies

Under the Proposal, the scope of income arising from transfer of domestic assets to a foreign company, which constitutes Korean-source “other income” and thereby is subject to 22% withholding tax (WHT) in Korea, has been expanded to include cases where assets are transferred for a significantly low consideration, specifically where the shortfall between the consideration paid and the fair market value is at least 30% of the fair market value.

2) Clarification of the scope of domestic source dividend income for foreign companies

There has been longstanding debate over whether payments equivalent to dividends, made to foreign companies under Total Return Swap (TRS) contracts based on domestic stocks, constitute dividend income subject to WHT. The Tax Tribunal previously ruled that such payments do not constitute dividends and are therefore not subject to WHT (Tax Tribunal Decision 2021Seo2050, April 18, 2024).

The Proposal would reverse this by including dividend-equivalent amounts from over-the-counter derivative transactions based on Korean stocks as Korean-source dividend income. Accordingly, TRS profits, where Korean stocks are the underlying asset, and paid to foreign companies, will be treated as Korean-source dividend income and subject to Korean WHT.

7. Improvements to the Application of the Foreign Tax Credit for Indirect Investment

1) Amendments for Individual Investors (Article 57-2(2), (3) of the Individual Income Tax Law)

For comprehensive income taxation, the indirect investment foreign tax credit for individual investors has been amended. Under the current system, the credit is calculated by multiplying the foreign CIT on indirect investments by the marginal tax rate applied to the comprehensive income tax base. Going forward, this method may be replaced with a revised approach that allows a deduction of an amount prescribed by Presidential Decree, taking into account the total amount of foreign CIT on indirect investments calculated at the time of withholding.

If enacted, this Proposal will apply to taxpayers filing income tax returns on or after January 1, 2026.

2) Rationalization for Corporate Investors (Article 15(2), 57-2(1)-(3) of the Corporate Income Tax Law)

Currently, under the Corporate Income Tax Law, foreign CIT paid through indirect investments is excluded both from the taxable base and from the tax credit limit calculation. As a result, such taxes are not effectively reflected in the tax credit limitation formula. Specifically, under the existing regime, the credit limit is determined as calculated tax amount × (total income from funds, etc. ÷ taxable income), which does not account for indirect foreign corporate tax.

The Proposals address this by incorporating eligible indirect foreign corporate tax amounts into taxable income under the Corporate Income Tax Law, thereby ensuring their inclusion in the tax credit calculation. At the same time, the limitation formula would be revised to calculated tax amount × (total income from funds, etc. + indirect investment foreign corporate tax) ÷ taxable income, thereby ensuring that indirect foreign CIT is fully reflected in the allowable credit.

If enacted, this Proposal will apply to companies filing tax returns for fiscal years beginning on or after January 1, 2026.

8. Introduction of Penalties for Failure to Submit Status Reports on Liaison Offices of Foreign Companies (Article 125 of the Corporate Income Tax Law)

The obligation for foreign companies to file status reports on their liaison offices was introduced at the end of 2021 and has been in effect since 2022 (Article 94-2 of the Corporate Income Tax Law). However, in the absence of penalties, there have been frequent cases of non-compliance.

To enhance the effectiveness of this reporting requirement, the Proposals introduce a penalty of up to KRW 10 million for non-compliance. Under the Proposals, such penalty applies to both non-submission and false submission of status reports, which must include information such as basic details of the liaison office, the status of the foreign headquarters and other domestic branches, and information on domestic business partners.

9. New Requirement to Submit Applications for Treaty-Based Reduced Tax Rates for Non-Residents (Article 156-6 of the Individual Income Tax Law, Article 207-8(8) of the Presidential Decree thereto, Article 98-6 of the Corporate Income Tax Law, Article 138-7(8) of the Presidential Decree thereto)

Currently, applications for the reduced WHT rates under tax treaties must be retained by the withholding agent for five years, but submission to the tax office is not required unless specifically requested by the tax office (Article 207-8(8) of the Presidential Decree of the Individual Income Tax Law, Article 138-7(8) of the Presidential Decree of the Corporate Income Tax Law).

Under the Proposals, withholding agents will be required to submit copies of such applications directly to the tax office by the end of February of the year following the year in which the income was paid, aligning the deadline with the submission of payment statements.

If enacted, this Proposal will apply to income paid on or after January 1, 2026.

10. Expansion of the Exit Tax to Overseas Stocks (Article 118-9 through 118-18 of the Individual Income Tax Law)

Under the current Individual Income Tax Law, when a resident departs Korea and becomes a non-resident from a taxation standpoint, any unrealized gains on domestic stocks held at the time of departure are deemed realized and taxed as capital gains under the exit tax provisions (Article 118-9).

The Proposals intend to expand the scope of this exit tax to cover foreign stocks (e.g., shares traded in the U.S.), reflecting the growing trend of Korean residents investing in foreign securities. That said, the Proposals have drawn considerable pushback from the expatriate community in Korea, as they may adversely affect the country’s ability to attract foreign talent (particularly in light of Korea’s aging population and low birth rate). It remains to be seen whether the new government will reconsider or withdraw the Proposals in response to these concerns.

If enacted, this Proposal will apply to individuals departing on or after January 1, 2027.

■ International Tax Coordination Law

11. Introduction of Domestic Minimum Top-up Tax under the Global Minimum Tax Framework (newly established Article 73-2 of the International Tax Coordination Law)

In line with the OECD’s Pillar 2 framework, Korea introduced the Income Inclusion Rule (IIR) and the Undertaxed Profits Rule (UTPR) as part of its global minimum tax regime on December 31, 2022. The IIR took effect on January 1, 2024, and the UTPR on January 1, 2025. The Proposals additionally call for the introduction of a Domestic Minimum Top-up Tax (DMTT).

The proposed DMTT is designed to conform with the OECD’s model rules and guidance, with the clear objective of obtaining recognition as a QDMTT through the Inclusive Framework’s peer review process. The domestic minimum tax will be calculated as:

[Minimum tax rate (15%) − Effective tax rate of domestic Constituent Entities] × Excess profits (GloBE Income – Substance-based income exclusion) + Current Additional Top-Up Tax Amount

Given that Korea’s statutory CIT rate (excluding local income tax) is 9-24% (10-25% under the Proposals), relatively few domestic companies are expected to fall below the 15% minimum threshold. However, where the effective tax rate is reduced through deductions or other reliefs, the DMTT may apply. Importantly, a QDMTT takes precedence over both the IIR and the UTPR.

If enacted, this new provision will apply to fiscal years beginning on or after January 1, 2026.

12. Additional Documentation Requirement for Tax Refund Claims Arising from Transfer Pricing Adjustments (Article 6(2) of the International Tax Coordination Law)

The current International Tax Coordination Law Article 7 authorizes the tax authorities to assess taxes based on arm’s length prices. Similarly, Article 6 of the International Tax Coordination Law allows taxpayers to request refunds on the same basis; however, the law does not explicitly require a corresponding adjustment in the counterparty jurisdiction as a condition for filing such a refund claim.

The Proposals introduce a new requirement that taxpayers must submit documentation demonstrating the existence of double taxation when filing a refund claim arising from transfer pricing adjustments. Accordingly, adjustments will only be permitted where double taxation actually arises due to the counterparty jurisdiction making a transfer pricing adjustment to the relevant transaction.

If enacted, this Proposal is scheduled to apply to claims filed on or after January 1, 2026.

13. Inclusion of Investment Trusts within the Scope of Residency Certificate Issuance (Article 41 of the International Tax Coordination Law)

Under the current Article 41 of the International Tax Coordination Law, only resident individuals and domestic companies are eligible to obtain residency certificates. Consequently, where residents or domestic companies made overseas investments through investment trusts (rather than through investment companies), residency certificates could not be issued in the name of the investment trust itself since a trust technically has no legal personality.

The Proposals address this discrepancy by allowing non-opaque investment vehicles (such as investment trusts, investment partnerships, and undisclosed investment associations under the Capital Markets Law) to obtain residency certificates, provided that all beneficial owners are Korean tax residents or domestic companies.

If enacted, this Proposal will apply to applications submitted on or after January 1, 2026.

■ Special Tax Treatment Coordination Law

14. Introduction of Separate Taxation on Dividend Income from High-Dividend Companies (newly established Article 104-27 of the Special Tax Treatment Coordination Law)

Low dividend payout ratios have often been cited as a factor contributing to the “Korea discount.” To address this, the Proposals introduce a new tax incentive mechanism aimed at encouraging higher dividend distributions. Listed companies (excluding public and private funds, real estate investment trusts, special purpose companies, etc.) that do not reduce their cash dividends compared to the previous year and meet one of the following criteria will qualify as high-dividend companies: i) a dividend payout ratio of 40% or more; or ii) a dividend payout ratio of at least 25% combined with an increase of 5% or more compared to the average of the preceding three years. Dividends from such companies will be exempt from comprehensive taxation of financial income, and instead be subject to separate taxation.

If enacted, this incentive will apply to dividends attributable to fiscal years beginning on or after January 1, 2026, and ending on or before December 31, 2028.

15. Introduction of Tax Exemption for Domestic Investment Income of the Bank for International Settlements (BIS) (Article 21(4), (5), and (6) of the Special Tax Treatment Coordination Law)

The Bank for International Settlements (BIS), an international financial institution that fosters cooperation among central banks, manages and invests funds deposited by central banks and international organizations worldwide. In Korea, its investments are currently limited to government bonds and currency stabilization bonds (CSBs), both of which are tax-exempt.

To facilitate broader investment in Korean won-denominated assets, the BIS has requested that income derived from deposits, repurchase agreements (RPs), derivatives, and other financial instruments also be exempt from taxation.

The Proposals, in order to support the BIS’ expansion of investment in won-denominated assets, expand the scope of tax exemptions under the Special Tax Treatment Coordination Law for interest income and other income derived from international financial transactions, to include the BIS’s domestic investment income (e.g., interest, dividends, and capital gains).

If enacted, this Proposal will apply to income generated on or after January 1, 2026.

16. New Tax Deferral for In-Kind Contributions of Foreign Subsidiary Shares to Foreign Companies (Article 38-3 of the Special Tax Treatment Coordination Law, Article 35-5 of the Presidential Decree thereto)

The Proposals introduce a new tax exemption mechanism to facilitate the restructuring of domestic companies’ overseas operations. Under this provision, domestic companies that contribute shares of foreign subsidiaries to a foreign company in-kind will be eligible for a tax deferral on the capital gains arising from such transactions. Specifically, if a domestic company that has been in continuous operation for at least five years contributes shares or equity interests of a foreign subsidiary (in which it holds a stake of 20% or more) to a foreign company in which the contributing company holds at least an 80% stake, the resulting capital gains will be deferred for four years and then recognized as income evenly over the following three years.

If enacted, this Proposal will apply to in-kind contributions made on or after January 1, 2026.

If you require assistance with any tax matters, including those related to the 2025 tax law amendment proposals, please feel free to reach out to the Lee & Ko Tax Group.